What Does “Medically Necessary” Mean — And Why Should You Care?

I learned what “medically necessary” meant the same way a lot of patients do: I overheard it. It wasn’t directed at me. It was part of a conversation happening nearby, clinical, clipped, matter-of-fact, and by the time I could have asked what it meant, the moment had passed. So I did what any of us do: I went home and Googled it.

What I found was a definition. What I needed was an explanation. Those are not the same thing.

If you’ve heard this phrase in a hospital room, on a phone call with your insurer, or buried in a denial letter you’re trying to decode, here’s what it actually means and why it matters more than most people realize.

The Official Definition (And Why It Only Gets You So Far)

According to HealthCare.gov, the federal government’s plain-language health insurance resource, medically necessary services are defined as:

“Health care services or supplies needed to diagnose or treat an illness, injury, condition, disease, or its symptoms and that meet accepted standards of medicine.”

That sounds reasonable. But notice what’s missing: who decides? That one short sentence is doing an enormous amount of work, and the gap between “medically necessary” as your doctor understands it and “medically necessary” as your insurance company defines it can be wide enough to drive a denial letter through.

The National Association of Insurance Commissioners (NAIC), the organization that helps regulate insurance practices across the country, offers a more complete picture in their consumer guide on medical necessity. According to the NAIC, most health plans define medically necessary services as those that are:

- Provided for the diagnosis, treatment, cure, or relief of a health condition, illness, injury, or disease

- Appropriate to the diagnosis, meaning the right type of care, at the right frequency, for the right duration

- Within generally accepted standards of medical care in the community

- Not primarily for the convenience of the patient, the patient’s family, or the provider

- Not experimental, investigational, or cosmetic in nature

Some plans add another filter: cost-effectiveness. If two treatments would work equally well, the cheaper one is typically the one your insurer considers medically necessary.

What’s Considered Not Medically Necessary?

This is where things get personal fast.

Insurers typically flag the following categories as outside the bounds of medical necessity:

- Cosmetic procedures, unless there’s a documented medical reason (some reconstructive surgeries, for example, may qualify)

- Experimental or investigational treatments, including some newer therapies that your doctor believes in but your insurer hasn’t caught up with yet

- Convenience-based care, such as getting a test done at a facility that’s easier for your schedule rather than the one your plan prefers

- Services that exceed standard guidelines, for example, therapy sessions beyond what utilization review allows, even if your provider believes you need more

- Treatments that aren’t supported by your diagnosis, meaning if the coding on your chart doesn’t match the procedure, coverage can be denied even if the care makes clinical sense

One thing worth understanding: when your insurer says something isn’t medically necessary, they often aren’t saying it won’t help you. They’re saying it doesn’t meet their criteria for reimbursement. Those are two different statements, and the distinction matters when you’re deciding whether to appeal.

Who Actually Decides?

Here’s the part nobody explains clearly.

Your doctor doesn’t get the final say. Neither do you.

A medical necessity determination is typically made by a utilization reviewer, someone who works for your insurance company and reviews your records against the plan’s internal medical policies. These policies are often based on guidelines from third-party clinical criteria tools. Your treating physician’s judgment is considered, but it’s not determinative.

The NAIC describes three types of reviews:

- Precertification (prior authorization): Happens before treatment. Your plan reviews the request and decides if it qualifies for coverage.

- Concurrent review: Happens during treatment, which is common with hospital stays, where insurers periodically check whether continued inpatient care is still warranted.

- Retrospective review: Happens after care has already been provided. Yes, they can decide after the fact that something wasn’t medically necessary and deny coverage accordingly.

Your doctor can submit a Letter of Medical Necessity to support a claim or an appeal. If you’re facing a denial, requesting this letter is one of the first things to ask your provider about.

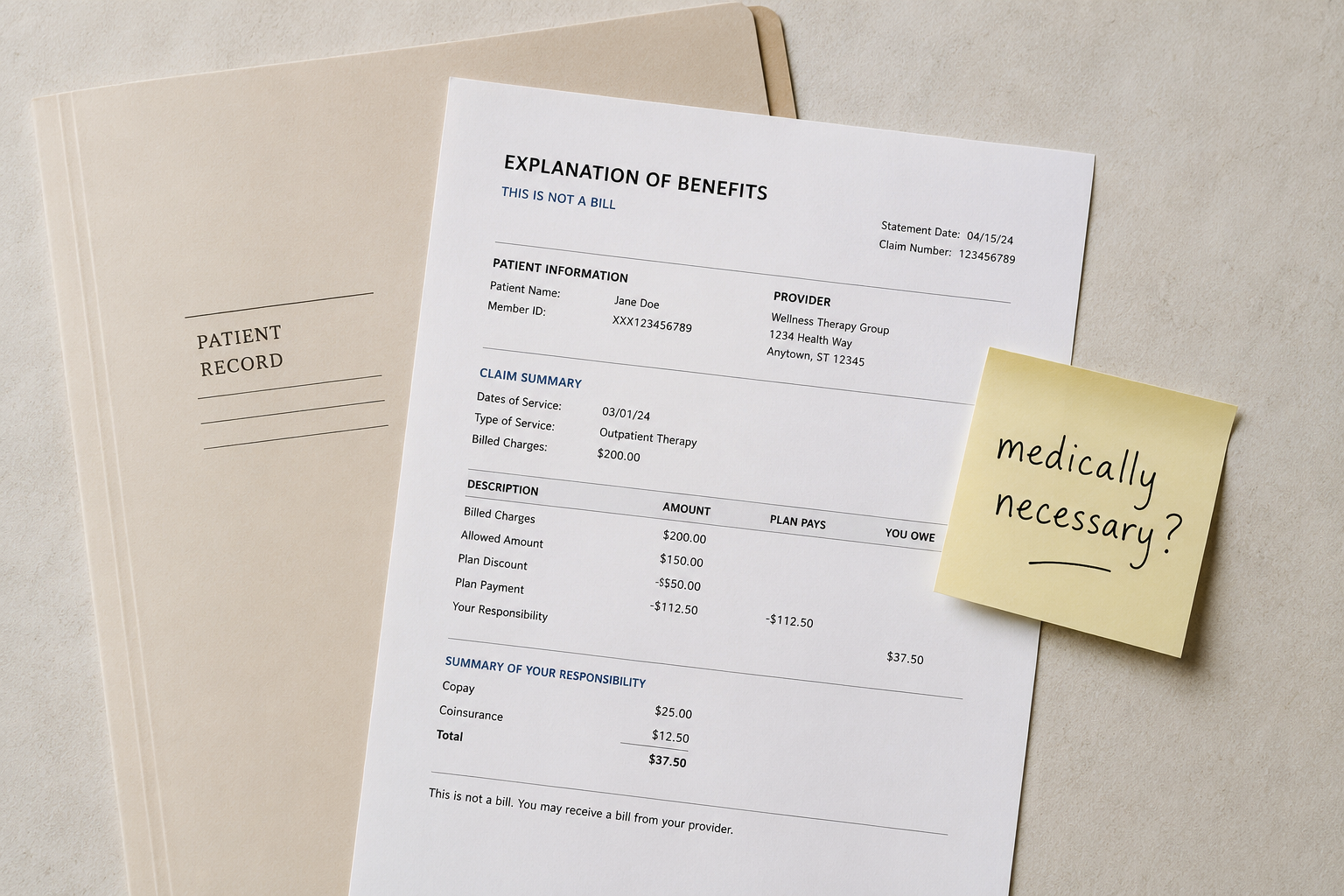

What’s an Example of a Medical Necessity Statement?

A Letter of Medical Necessity is typically written by your treating provider and submitted to your insurance company. It generally includes:

- Your diagnosis (with ICD codes, the numerical shorthand used for billing)

- The specific treatment or service being requested

- Why that treatment is appropriate for your specific condition

- What alternatives were considered, and why this option is clinically preferred

- Supporting evidence from published medical literature, if applicable

You won’t write this letter yourself, but you can ask your provider to write one, and you can ask to see a copy. If you’re appealing a denial, this document is often central to the case.

Does “Medically Necessary” Apply If You Don’t Have Insurance?

This is the question that doesn’t show up in most explainer articles, and it deserves a direct answer.

The short version: the phrase “medically necessary” exists inside insurance contracts. It’s a coverage term, not a medical standard. If you don’t have insurance, no one is using this phrase to gatekeep your care, but the concept still echoes in ways that affect you.

Here’s how:

Pricing and billing: Hospitals and providers use medical necessity coding to determine what to charge and how to categorize your care for billing purposes. Uninsured patients still receive itemized bills that reflect these categories.

Financial assistance eligibility: Many hospital systems offer discounted or charity care for uninsured patients, specifically for medically necessary services. Cosmetic or elective procedures that aren’t medically necessary typically don’t qualify for the same assistance. Mayo Clinic, for example, explicitly notes that its uninsured discount applies to medically necessary care, not elective or cosmetic procedures.

Medicaid eligibility: If you’re uninsured and seeking retroactive Medicaid coverage for a hospitalization, medical necessity documentation can affect whether that coverage is approved.

Emergency care: Under federal law (EMTALA), hospitals that accept Medicare must stabilize patients regardless of insurance status. Emergency departments can’t demand proof of coverage before treating you. But “stabilizing” doesn’t mean the full scope of treatment your provider might recommend, and once you’re stable, the coverage questions begin.

The bottom line: if you’re uninsured, you won’t receive a denial letter citing medical necessity. But the same clinical coding that determines necessity is still being applied behind the scenes, shaping your bill, your assistance eligibility, and your access to follow-up care.

What Falls Under “Medically Necessary”?

If you’re wondering whether a specific service qualifies, the honest answer is: it depends on your plan. But the following types of care generally meet the threshold across most definitions:

- Diagnostic tests ordered to investigate documented symptoms

- Prescription medications for a confirmed diagnosis

- Surgery to treat a diagnosed condition

- Mental health treatment (federal parity laws now require insurers to evaluate mental health necessity by the same standards as physical health)

- Inpatient hospitalization when outpatient care isn’t sufficient

- Durable medical equipment (wheelchairs, CPAP machines, etc.) with appropriate documentation

- Physical, occupational, or speech therapy tied to a specific diagnosis and treatment plan

What often falls outside the definition, even when it feels necessary to you and your provider:

- Preventive testing beyond what standard guidelines recommend for your age and risk profile

- Off-label medication use without documented evidence of effectiveness for your specific condition

- Second opinions at out-of-network facilities

- Extended inpatient stays when the insurer determines outpatient care would be adequate

Why This Phrase Is Worth Knowing

“Medically necessary” isn’t just insurance jargon. It’s the phrase that determines whether a bill becomes your problem or your insurer’s. It’s used in denial letters, in prior authorization requests, in hospital discharge planning conversations, and in appeals. It’s applied to mental health care, prescription coverage, emergency services, and elective procedures.

It’s also a phrase that gets deployed around patients rather than explained to them, which is how many of us end up in the position I was in: standing on the outside of a conversation, catching a phrase mid-sentence, and realizing we don’t have the vocabulary to ask the right question.

Now you do.

If You’ve Been Denied: What to Do Next

If a claim has been denied as “not medically necessary,” you have options:

- Request the denial in writing if you haven’t received it. You’re entitled to a written explanation.

- Review your plan’s definition of medical necessity. It’s in your Evidence of Coverage or Summary Plan Description. The NAIC recommends checking this document to understand what standard your plan applies.

- Ask your provider for a Letter of Medical Necessity if they haven’t already submitted one.

- File an internal appeal with your insurer. Most plans have a defined appeals process with a deadline, often 30 to 180 days from the denial.

- Request an external review if your internal appeal is denied. Under the ACA, you have the right to have your case reviewed by an independent organization, and their decision is binding on the insurer.

- Contact your state insurance commissioner if you believe the denial is unjustified. The NAIC maintains a directory of state insurance regulators at naic.org.

Sources:

Read Your Own Chart is a patient advocacy resource published under Intrinsic Vicissitude LLC. Nothing here is legal or medical advice — it’s what you should have been told at your doctor’s office.